US funding markets see $120B influx as structural shifts reshape bank liquidity

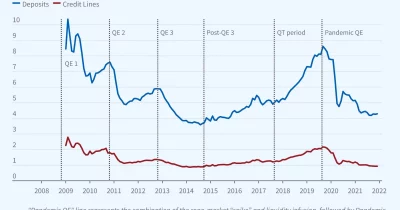

A $120 billion influx into US money market funds is reshaping bank liquidity dynamics, potentially constraining funding availability for smaller financial institutions. This structural shift reflects changing investor preferences and has significant implications for banking sector stability and credit availability.

The $120 billion movement into money market funds represents a meaningful reallocation of capital within US funding markets, signaling investor confidence in short-term fixed-income instruments amid broader economic uncertainty. Money market funds have historically served as safe havens during periods of market volatility, and this substantial inflow suggests investors are reassessing risk across their portfolios and seeking liquid, stable returns rather than longer-dated assets or equities.

This capital migration stems from multiple structural factors: rising interest rates have made money market yields more attractive relative to other short-term investments, regulatory changes affecting bank reserve requirements, and lingering concerns about regional banking stability following recent bank failures. The post-2023 banking crisis created persistent wariness among depositors and institutional investors regarding bank safety, accelerating the shift toward alternative liquid instruments.

The concentration of liquidity in money market funds directly impacts smaller regional and community banks that traditionally rely on retail deposits and wholesale funding markets. As capital flows toward money market funds, these institutions face tighter funding conditions, higher borrowing costs, and potential constraints on credit expansion. This creates a two-tiered banking system where larger institutions with diversified funding sources maintain stability while smaller competitors struggle with liquidity costs.

Looking ahead, policymakers and market participants should monitor whether this trend continues and whether the Federal Reserve adjusts policy to address potential credit market tightening. The sustainability of this inflow depends on interest rate trajectories and broader economic conditions. If money market rates decline while equity markets stabilize, capital could reflow to riskier assets, easing pressure on smaller banks.

- →$120 billion influx into money market funds reflects structural shifts in US funding markets and investor preferences

- →Smaller banks face tightened liquidity conditions as capital migrates away from traditional banking deposits

- →Rising money market yields and banking sector concerns drive investor demand for safer, liquid instruments

- →The trend could create a two-tiered banking system favoring larger institutions with diversified funding sources

- →Future interest rate movements and economic stability will determine whether this capital reallocation persists