Private-credit firms report decline in returns amid Fed rate cuts

Private-credit firms face declining returns as Federal Reserve rate cuts compress yields, while simultaneously confronting risks of elevated default rates. This margin squeeze threatens profitability across the sector and has broader implications for credit availability and risk management in non-traditional lending markets.

The private-credit sector confronts a structural profitability challenge as monetary policy shifts toward rate cuts. When the Federal Reserve reduces benchmark interest rates, lenders face immediate pressure on net interest margins—the spread between borrowing costs and lending yields. Private-credit firms, which typically target higher returns than traditional banks by lending to less-creditworthy borrowers, find their yield advantage eroding just as portfolio risks intensify. This creates a dual squeeze: lower rates compress revenue while economic slowdown typically correlates with rising defaults, increasing loss reserves and reducing net earnings.

This dynamic reflects broader macroeconomic headwinds. During periods of sustained higher rates, private-credit managers benefited from generous spreads compensating them for credit risk. As the Fed pivots to accommodation, that cushion diminishes precisely when credit cycles typically deteriorate. The sector's growth over the past decade depended partly on an attractive risk-return tradeoff for institutional investors; compressed yields make that proposition less compelling.

For institutional investors and pension funds that have allocated capital to private-credit strategies, this signals potential underperformance relative to historical benchmarks. Asset managers may respond by reducing new commitments, tightening underwriting standards, or shifting toward higher-risk borrowers to maintain target returns—each carrying distinct dangers. The broader credit market could contract if private-credit providers pull back, reducing financing options for mid-market companies and leveraged buyouts.

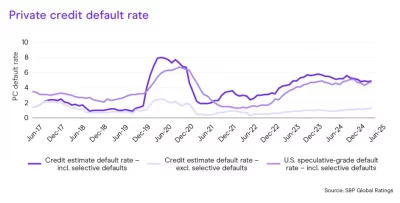

Investors should monitor default rate trends in existing portfolios and track capital deployment rates by major managers. Fund valuations and secondary-market pricing will reveal how the market reprices private-credit risk under the new rate regime.

- →Fed rate cuts directly compress net interest margins for private-credit lenders, squeezing profitability

- →Rising default risks coincide with declining yields, creating a simultaneous revenue and loss reserve challenge

- →Institutional investors may reduce allocations to private-credit strategies as risk-adjusted returns deteriorate

- →Private-credit managers may increase underwriting risk or target riskier borrowers to maintain target returns

- →Secondary market pricing and default rate trends will be critical indicators of sector stress ahead