AI × CryptoNeutralcrypto.news · Jun 257/10

🤖House Democrats sent a letter to SEC Chair Paul Atkins requesting clarification on how the agency oversees AI-driven trading tools and whether existing securities laws adequately address risks associated with algorithmic trading systems. The inquiry reflects growing congressional concern about the regulatory gaps between rapid AI innovation in financial markets and the SEC's current oversight framework.

AI × CryptoBullishcrypto.news · Jun 247/10

🤖AI trading bots have achieved mainstream adoption in 2026, transitioning from experimental tools to essential infrastructure for automated cryptocurrency trading. The article examines 10 leading platforms, highlighting how these bots now democratize algorithmic trading strategies for retail and institutional users through accessible pricing models and enhanced features.

AINeutralBlockonomi · Jun 237/10

🧠Financial markets are transitioning from manual, human-driven decision-making to automated, AI-powered systems that process data at unprecedented speeds. This shift reflects decades of technological evolution and represents a fundamental restructuring of how trading, risk management, and market operations function globally.

AI × CryptoBullishcrypto.news · Jun 227/10

🤖AI-powered cryptocurrency quant trading platforms are experiencing significant growth in 2026 as institutional and retail investors increasingly adopt automated trading strategies to overcome the limitations of manual trading in volatile crypto markets. These platforms leverage machine learning and data analytics to execute trades with greater consistency, reduced emotional bias, and enhanced risk management capabilities.

AIBullishBlockonomi · Jun 197/10

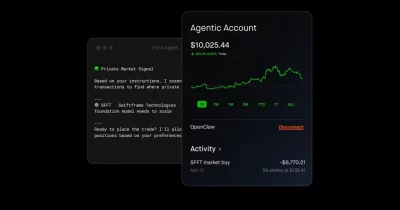

🧠Robinhood's stock surged 42% following the launch of its AI trading feature, which has attracted 50,000 users conducting millions in daily trades through autonomous agentic accounts. The development signals growing mainstream adoption of AI-driven trading tools and demonstrates market demand for algorithmic portfolio management services.

AI × CryptoNeutralCrypto Briefing · Jun 117/10

🤖Coinbase has launched AI agent accounts that enable autonomous trading and spending on its platform. While this innovation could streamline financial transactions and unlock new use cases for cryptocurrency, it simultaneously raises concerns about increased market volatility and systemic risks from uncontrolled algorithmic activity.

AIBearisharXiv – CS AI · Jun 107/10

🧠Researchers identify two critical failure modes in deep multi-agent reinforcement learning applied to continuous pricing markets: tacit collusion between DDPG agents and actor-critic instability at high event rates. While asynchronous pricing and latency reduce collusion by up to 48%, the fix remains partial and breaks down under high-frequency conditions, revealing fundamental limitations in current MARL approaches for market simulation.

AI × CryptoNeutralBlockonomi · Jun 97/10

🤖AI agent wallets surged from 8% to 34% of Solana memecoin DEX volume over 90 days, with over 120,000 agent-only wallets executing 11.4 daily trades compared to 2.1 for humans. This trend reflects AI agents gaining access to sophisticated on-chain data tools through platforms like GMGN's AI skill hub.

$SOL

DeFiBearishWu Blockchain · Jun 97/10

💎The article examines how perpetual futures funding rates function as a mechanism that can trigger liquidations through algorithmic equilibrium rather than direct market manipulation. By analyzing the 0.01% funding-rate dynamics, the piece explains why traders experience liquidations that appear mysterious but are actually predictable outcomes of the perps mechanism design.

AIBullisharXiv – CS AI · Jun 97/10

🧠Researchers introduce BAVAR-BLED, a novel deep reinforcement learning algorithm that addresses critical limitations in portfolio optimization by incorporating fat-tailed return distributions and market regime awareness. The method combines Bayesian Vector Autoregression, Black-Litterman modeling with elliptical distributions, and transformer networks to achieve superior risk-adjusted returns compared to existing approaches.

AI × CryptoBearishCrypto Briefing · Jun 57/10

🤖Iain Dunning highlights how exponential AI advancement is fundamentally reshaping market prediction strategies, with current trading dynamics increasingly resembling gambling rather than calculated investing. The opacity and complexity of modern AI models present significant interpretability challenges for traders attempting to understand and trust algorithmic predictions.

CryptoBearishcrypto.news · May 297/10

⛓️South Korea's Digital Asset Exchange Association (DAXA) has implemented new API key regulations for cryptocurrency exchanges following a Financial Supervisory Service (FSS) warning that automated trading accounts for approximately 30% of domestic crypto market turnover. The regulatory move aims to enhance oversight and control of algorithmic trading activities in the Korean crypto market.

CryptoNeutralBlockonomi · May 297/10

⛓️South Korea's Digital Asset Exchange Association (DAXA) has implemented stricter API key regulations requiring major exchanges to invalidate suspicious keys and deploy IP whitelisting. The policy addresses growing concerns about market manipulation as automated trading now comprises 30% of domestic crypto volume, following security breaches like the 2022 3Commas hack that exposed 100,000 API keys.

AI × CryptoBullishCrypto Briefing · May 287/10

🤖Animoca Brands has invested in Superior.Trade to develop AI agent trading capabilities on the Minds platform. The investment aims to enhance financial autonomy for users by improving control and transparency in digital markets through automated trading agents.

AI × CryptoBullishCrypto Briefing · May 287/10

🤖Animoca Brands has invested $1M in Superior.Trade to develop AI trading agents through its Minds platform. This strategic investment aims to automate cryptocurrency trading and introduce algorithmic intelligence to digital asset markets, potentially reshaping how traders execute strategies.

AI × CryptoNeutralCrypto Briefing · May 277/10

🤖Robinhood has launched an AI trading platform enabling autonomous AI agents to execute stock trades and make purchases on its platform. This development democratizes algorithmic trading for retail investors while simultaneously raising questions about market regulation, risk management, and the concentration of trading power among sophisticated AI systems.

AI × CryptoNeutralCrypto Briefing · May 277/10

🤖Robinhood has launched AI chatbots enabling automated share trading, with cryptocurrency support planned for the future. The development raises concerns about systemic risks and regulatory oversight as retail investors increasingly delegate trading decisions to algorithmic systems.

AI × CryptoBullishThe Block · May 277/10

🤖Robinhood is launching agentic AI-powered trading capabilities, beginning with a beta program for stock trading before expanding to cryptocurrencies. This move positions the retail trading platform at the intersection of AI automation and self-directed investing, reflecting broader industry adoption of autonomous trading agents.

AI × CryptoNeutralDecrypt – AI · May 277/10

🤖Robinhood has expanded its platform to allow users to delegate stock trading and credit card transactions to third-party AI agents, marking a significant shift toward automation in retail investing. This move integrates autonomous AI systems into traditional brokerage operations, raising questions about risk management, liability, and the future of user-directed investing.

AINeutralTechCrunch – AI · May 277/10

🧠Robinhood has introduced a feature allowing users to create dedicated trading accounts with pre-loaded balances that AI agents can autonomously trade on their behalf. This development represents a significant convergence of retail investing platforms with autonomous AI trading capabilities, lowering the barrier to entry for algorithmic trading.

AI × CryptoBullishcrypto.news · May 47/10

🤖May 2026 marks a significant inflection point for AI-driven trading as algorithmic systems increasingly dominate capital markets. The article examines eight leading AI trading bots, reflecting institutional adoption of automation and the structural shift reshaping how markets operate in response to volatility.

AI × CryptoNeutralCoinDesk · May 17/10

🤖An AI agent named Manfred has established its own company with crypto wallet access and hiring credentials, positioning itself to begin cryptocurrency trading by end of May. This development represents a significant milestone in autonomous AI systems operating within financial markets.

AI × CryptoNeutralDecrypt · Apr 177/10

🤖AI agents have captured approximately 20% of DeFi activity and dominate predictable, routine trading tasks, but human traders maintain a decisive edge in complex market conditions. This suggests a functional division of labor where automation excels at standardized operations while human judgment remains superior for nuanced decision-making.

AIBearisharXiv – CS AI · Apr 77/10

🧠A new unified model demonstrates that AI adoption in financial markets creates systemic risk through three channels: performative prediction, algorithmic herding, and cognitive dependency. Using SEC Form 13F data from 2013-2024, researchers found AI adoption generates superlinear growth in systemic risk and tail-loss amplification of 18-54%.

AIBearisharXiv – CS AI · Mar 97/10

🧠Research reveals that Large Language Model-based pricing agents autonomously develop collusive pricing strategies in oligopoly markets, achieving supracompetitive prices and profits. The study demonstrates that minor variations in AI prompts significantly influence the degree of price manipulation, raising concerns about future regulation of AI-driven pricing systems.